conceptual framework 2

Concepts of Microfinance Institutions

Although the definitions of microfinance institutions provided by many writers and organisations appear to differ, they are fundamentally identical.

Microfinance is defined as the provision of financial services, especially savings and loans, to low-income people without access to commercial banks (Arsyad, 2005). Microfinance institutions, according to Otero (1999), provide financial services to low-income and self-employed individuals at the household level. Savings, credit, insurance, payment, and money transfer services are all examples of financial services (Ledgerwood, 1999).

Microfinance institutions are defined by Schreiner and Colombet (2001) as « the attempt to improve access to small deposits and small loans for poor households neglected by banks. »

As a result, in this study, microfinance institutions are defined as businesses that provide financial services like as savings, loans, and insurance to low- income persons living in both urban and rural regions who are unable to acquire such services through the official financial sectors.

Financial Performance Indicators

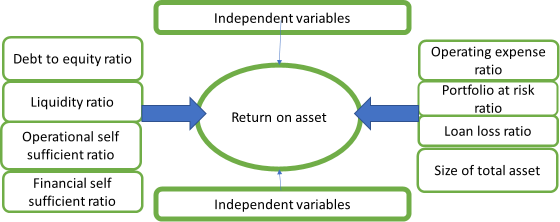

Institutional financial performance is judged in terms of profitability and success in creating wealth from invested capital. Institutional profitability may therefore be quantified in terms of Return on Assets (ROA) and Return on Equity (ROE). ROA is a percentage that represents generated net income in relation to total assets used to create net income. ROA is calculated as net income minus donations divided by average total assets. It is a ratio that assesses an institution’s total financial performance or profitability by taking into account both the profit margin and efficiency.

Furthermore, it indicates the extent to which management is efficient in creating earnings from investment. Return on assets is more basic and inclusive than return on equity since return on equity only measures profitability in terms of partial invested capital, for instance there is equity, while disregarding cost of funding and operational efficiency.

3.8. Empirical Studies

Various studies on microfinance organisations have been conducted by experts all around the world. Trong (2012) investigated capital structure and the financial performance of microfinance institutions. The study looked at the relationship between funding and microfinance performance and came to the conclusion that profitable and better regulated microfinance institutions are more sustainable, efficient, and reachable.

Jordan (2008) examined the effects of macroeconomic environment factors on the sustainability of 85 Latin American microfinance institutions. The findings indicate that none of the macroeconomic factors have a substantial influence on the repayment rate. However, per capita GDP has a significant impact on ROE. Dissanayake (2012) attempted to analyse the profitability drivers of microfinance institutions in Sri Lanka. The data suggest that debt to equity and operational expenditure ratios have a negative relationship with ROE. The write-off ratio and cost per borrower ratio, on the other hand, have a considerable positive association with ROE. Personnel productivity ratio, on the other hand, is not a statistically significant factor of ROE.

Gibson (2012) also did a study in Kenya titled « determinants of operational sustainability of microfinance institutions. » According to the findings, the capital/asset ratio and operational expenses/loan portfolio are the elements that influence operations and financial sustainability. The study also advised that these indicators be combined with operational self-sufficiency to develop a sustainability index.

On the other hand, few research on the financial performance of microfinance organisations have been undertaken in Ethiopia. Melkamu (2012) investigated the factors influencing the operational and financial self-sufficiency of

Ethiopian microfinance organisations. The study found that MFIs age has a favourable but small influence on their financial performance, whereas portfolio at risk, gearing ratio, and market concentration have a negative but minor effect.

Furthermore, Muhidin (2015) indicates that growing reliance on donor funding undermines sustainability, whereas keeping a larger percentage of deposits as a percentage of loans leads to enhanced microfinance organisation sustainability.